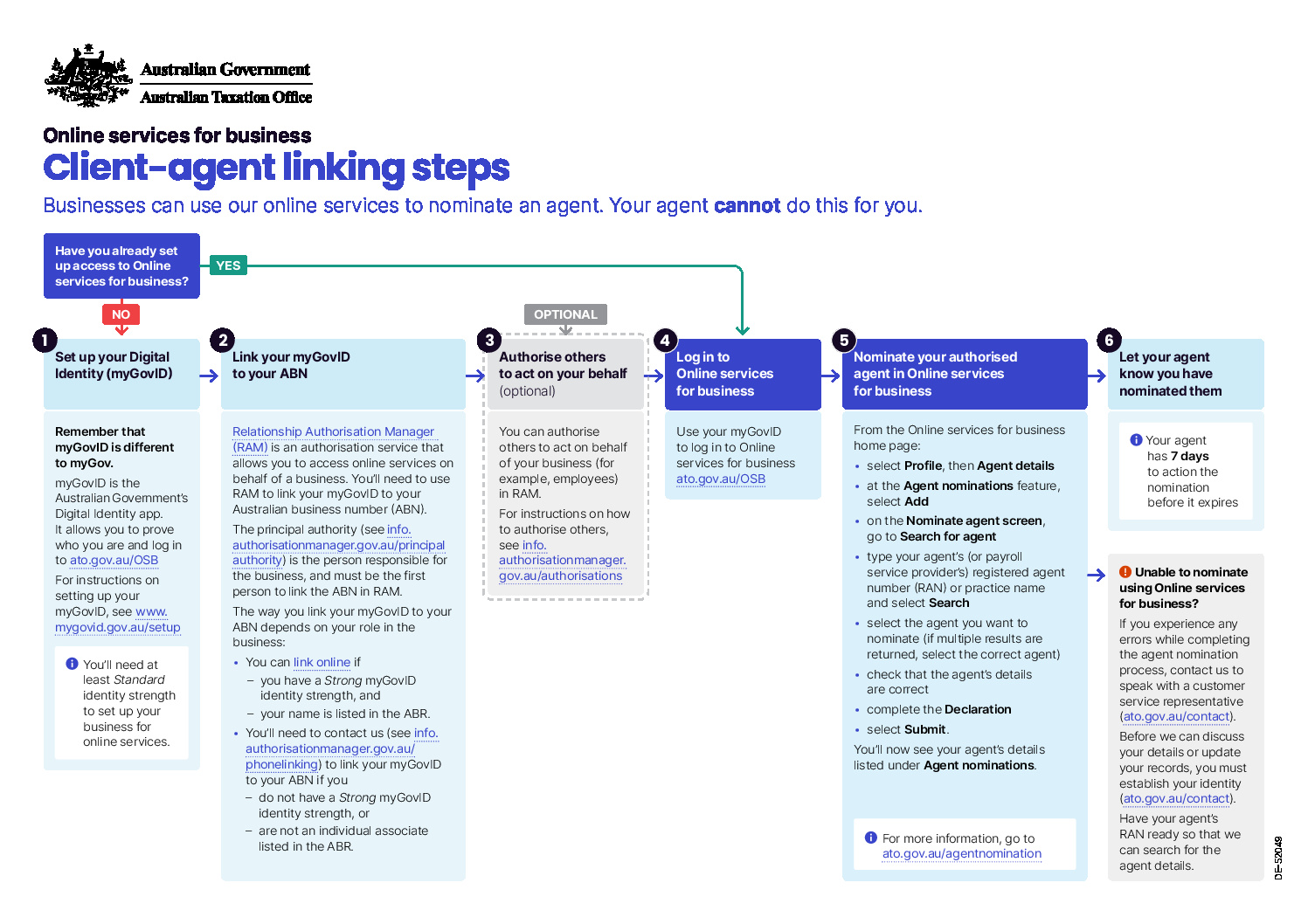

The US Federal Reserve lifted interest rates by a quarter of a percent this week. According to normal expectations this was supposed to result in:

- Falling stock prices

- Rising bond yields

- Rising dollar and;

- Falling gold prices.

Guess what happened? None of the above. In fact, in all four assets the opposite happened.

- Stocks rose by almost 1%.

- The 10-year bond went from 2.6% down to 2.5%.

- The US dollar fell by more than 1% against the Euro and Yen and almost 2% against the Australian dollar.

Rising interest rates were supposed to make the US dollar stronger! And rising interest rates were supposed to make gold less attractive. Yet gold rallied by $20 or 1.7% on the night.

All four of those major markets went the opposite direction to what economic theory would tell you.

Why is this so?

It’s all about ‘buy the rumour – sell the fact’.

When an event is expected so widely as this Fed rate hike was, traders get themselves positioned well before the event. Sometimes the trade is so crowded that once the rumour becomes fact, everyone is positioned on the same side of the trade.

The interest rate rise at this month’s Fed meeting was indeed widely expected.

The minutes of the meeting confirmed what we had been thinking for some time, that interest rates, whilst increasing, would be at a moderate pace compared to previous cycles.

The global debt load, which has only increased since the GFC, means any little ‘pull of the lever’ (moving interest rates) can have a big effect, and as a result central banks around the world will continue to be cautious about the pace of raising interest rates.

What next?

Based on the market reaction to the Fed increase on March 15, we would expect that another two rate hikes this year in America could be absorbed without requiring the Reserve Bank of Australia (RBA) to make any increases at all.

We suspect the RBA would like to raise interest rates to fire shots across the bow of property investors, reminding them that rates can go up as well as down, before speculation gets out of hand. However the still weak economy and the risk of pushing the dollar higher is likely preventing that in the short-term. APRA and the RBA are more likely to wait and see if there are some adjustments to negative gearing and CGT in the budget to rein in property speculation.

What’s the lesson?

The lesson from the market reaction to the Fed rate increase is that positioning is best done well before market events. Market participants tend to look at least 6 months ahead and get well positioned before announcements of things like GDP and inflation numbers, and often when the expectations are correct, markets move opposite to what might be expected, because the marginal buyer and seller is already well positioned for the event.